Borrowing for Holidays

As we head towards the silly season after a long year of hard work, a holiday is something we all desire. However what can provide us with a few weeks of absolute bliss, can also end up costing a fortune over the long term if we don’t fund it right.

The best way to fund a holiday is of course through your savings. It’s what happens when you don’t have any savings and you decide to borrow to fund your holiday is where things can get messy.

The worst way to fund a holiday would be through a credit card as it has the highest amount of interest payable.

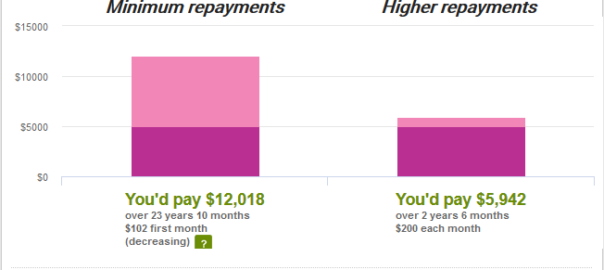

Based on a borrowed amount of $5,000 and an interest rate of 14.99%, if you paid the minimum amount each month, it would take you over 23 years and 10 months to pay it back with a total cost of the holiday of $12,018. More than twice what the actual holiday cost!

Source: MoneySmart.gov.au

By making increased payments of $200 per month, the amount would be paid off in 2 and a half years and would cost you $5,942. Keep in mind however that yes, you’ve saved $6,077 over the long term by paying off more than the minimum required, however even still the holiday is costing you nearly 20% more than the actual cost of the holiday.

With larger overseas holidays the numbers are even worse as the more you borrow, the more likely you are to be making the minimum monthly repayments as that is most likely all you can afford. That $20,000 holiday can quickly become a $40,000 holiday. You’ve effectively paid for 2 holidays but only received 1.

Another tempting option is to redraw on the home loan for your holiday as the interest rates are a lot cheaper. The below analysis shows the cost of borrowing $20,000 at 5.50% over 20 years.

Source: MoneySmart.gov.au

While the minimum payment will take you 19 ½ years to pay off, by paying approximately twice the minimum amount, you reduce the term of the loan by nearly 13 years and save approximately $9,500 but even then it will take you nearly 7 years to pay off your holiday, long after most of the memories have faded.

We all enjoy holidays and while it can be tempting to borrow money to fund them, a much better alternative is to plan ahead and save money before you go on holiday. If you haven’t yet saved up enough to fund your holiday, why not try some alternatives such as staying home and doing some day trips over summer, a cheap camping trip, delaying your holiday until less peak (and therefore cheaper) times of the year or even skipping this year and going on holiday next year when you can afford it.

Over the long term, using your savings rather than borrowing will enable you to go on holidays more frequently. At JBS it’s not only about saving for retirement, we also help you save for your holidays.

– Liam Rutty –