5 common financial mistakes to avoid during a crisis

The economic impact of the COVID-19 pandemic is playing havoc with finances for many households. In an ideal world, the financial boost should be enough and assumes that everyone was financially prepared for tough times. But in times of crisis, it can all be a little overwhelming.

The economic impact of the COVID-19 pandemic is playing havoc with finances for many households. In an ideal world, the financial boost should be enough and assumes that everyone was financially prepared for tough times. But in times of crisis, it can all be a little overwhelming.

Here are 5 common financial mistakes to avoid during a crisis and help you get to the other side with minimal money stress:

- Not paying attention to the household finances

According to a study by Deloitte Access Economics, a worrying 14 per cent of Aussies struggle to pay their bills (including rent, mortgage, utilities and credit cards). The study found that 26 per cent are spending more than they earn and live from pay cheque to pay cheque. Taking time to pay a little more attention to your household budget will help you stay afloat financially and not fall into unnecessary debt.

Start by listing all discretionary spending and reduce non-essential spending as much as you can. Identify those recurring direct debits to subscription services you no longer use. Perhaps home cooking will do rather than Uber Eats. Schedule a payment plan with essential providers such as utilities and rates. Discuss holiday repayment options with your bank or landlord.

Try using a spreadsheet or budgeting app to make it easier to track your spending during this time. You’ll quickly get a true picture of your financial health.

- Not building up emergency funds

The Deloitte study also found 13.4 million Aussies don’t have emergency savings to fall back on if they are out of a job. While we could not have predicted a pandemic, it certainly has exposed the financial vulnerability of not ‘saving for a rainy day’. A general rule of thumb is keeping aside three to six months of living expenses.

With banks letting borrowers hit pause on their home loan repayments, and as many as 375,000 individuals applying for the repayment relief, saving any excess surplus into an emergency fund to cover delayed repayments will see you in a stronger financial position.

- Making emotional investment decisions

Share market volatility has seen global markets bounce around, resulting in lower investor confidence. With markets falling as much as 37 per cent, you may be thinking of abandoning your long-term investment strategy and cashing in your portfolio. However, share markets have proven that a recovery follows a crisis. The Global Financial Crisis of 2007 and the Black Monday Crash of 1987 are good examples. So, it makes sense to stay the course with a quality investment strategy whilst reviewing it regularly in line with financial goals.

- Assuming your estate is in order

Half of Australians do not have a will. Of these, 34 per cent said they ‘haven’t got around to it.’ Without a valid will, your estate affairs end up in chaos. In light of the current pandemic which can have fatal consequences, setting up your estate affairs should be high on your list. A simple will can be drafted up by a lawyer for as little as the cost of smart TV.

- Not seeking professional advice

In times of financial crisis, it might seem more affordable to take a ‘Do-It-Yourself’ approach to save on costs, rather than seek the advice of a financial advice professional. During COVID-19 crisis, the Australian Government eased the rigid regulatory requirements to allow more access to professional advice. Working alongside a subject matter expert such as a financial planner, may help you achieve a better financial outcome as well as putting your mind at rest about the future.

Reach out to the JBS Financial to help to discuss your situation.

Source: Money and Life

While it’s impossible to anticipate future changes to the global economy, there’s plenty you can do to help prepare your personal finances for an unpredictable future. A new financial year is a great time for a check-up and to set yourself new financial goals.

While it’s impossible to anticipate future changes to the global economy, there’s plenty you can do to help prepare your personal finances for an unpredictable future. A new financial year is a great time for a check-up and to set yourself new financial goals.

Financial wellbeing is often overlooked as one of the pillars of good health, but it’s every bit as important as your physical, mental and emotional health.

Financial wellbeing is often overlooked as one of the pillars of good health, but it’s every bit as important as your physical, mental and emotional health.

Super is different from other assets, such as your house, because the trustee of your super fund ultimately decides who gets your super and any associated life insurance, if it’s held within the super fund, when you die.

Super is different from other assets, such as your house, because the trustee of your super fund ultimately decides who gets your super and any associated life insurance, if it’s held within the super fund, when you die.

The COVID-19 crisis has seen many Australians taking steps to stay afloat with their finances. With women more likely than men to withdraw super to make up the shortfall in their income, what does this mean for their long-term financial wellbeing?

The COVID-19 crisis has seen many Australians taking steps to stay afloat with their finances. With women more likely than men to withdraw super to make up the shortfall in their income, what does this mean for their long-term financial wellbeing?

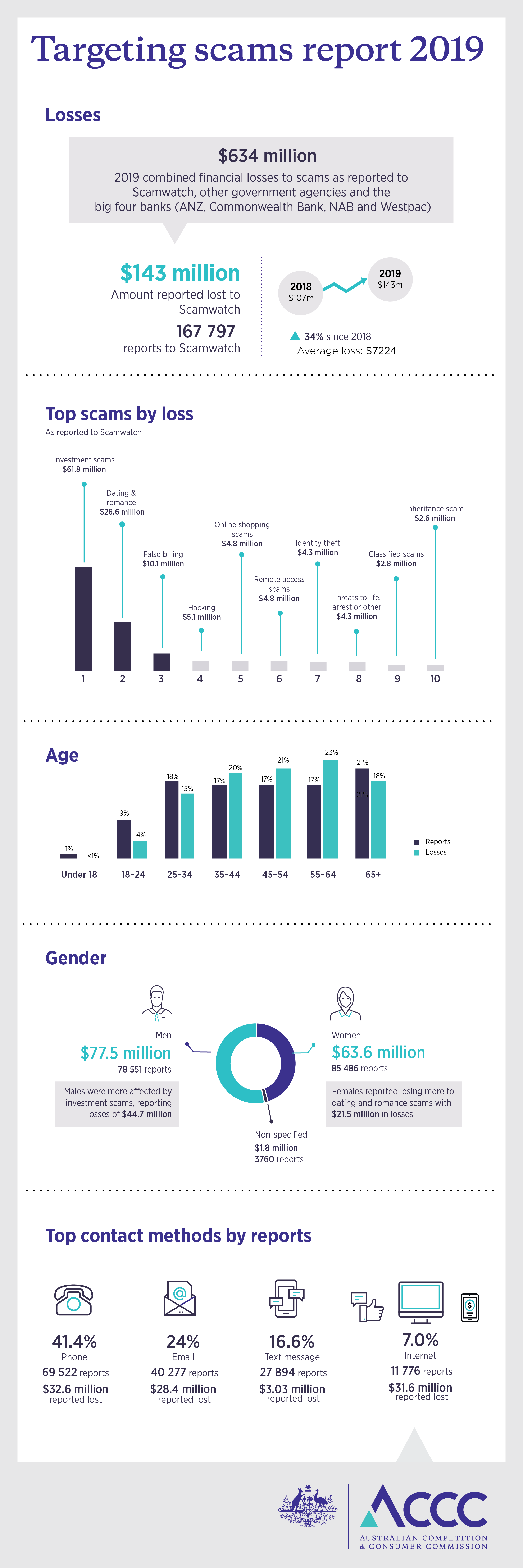

There were more than 353,000 combined reports to Scamwatch, other government agencies and the big four banks last year.

There were more than 353,000 combined reports to Scamwatch, other government agencies and the big four banks last year. Business email compromise scams accounted for the highest losses in 2019, with the Australian business community, and some individuals losing $132 million.

Business email compromise scams accounted for the highest losses in 2019, with the Australian business community, and some individuals losing $132 million.

This not only allows retired people to have access to more money to fund their retirement, it’s also likely to have freed up new property for sale for first home buyers and young investors.

This not only allows retired people to have access to more money to fund their retirement, it’s also likely to have freed up new property for sale for first home buyers and young investors.

Just like your physical health, the more you can monitor what’s happening with your finances, the easier it will be to improve your financial fitness.

Just like your physical health, the more you can monitor what’s happening with your finances, the easier it will be to improve your financial fitness.