How you can significantly increase your retirement savings

A transition to retirement (TTR) pension enables Australians who have met preservation age (currently 55) to access their super in the form of a pension. TTR’s were introduced in July 2005 to help Australians transition to retirement by topping up their income as they moved from full-time employment to part-time employment.

Although some people use TTR’s for their intended purpose, many use them as a way to top up their retirement savings. Below are three key benefits of this strategy, with a focus on combining it with a salary sacrifice strategy.

You pay zero tax on earnings within a TTR pension

Like most super pensions, the tax rate on earnings within a TTR pension is zero, compared with 15% within the superannuation accumulation (contribution) phase. For example, assuming a $1,000,000 balance and a 6% return on this investment, this equates to a $9,000 tax saving per year.

Income from a TTR pension is concessionally taxed

Income from a TTR pension is concessionally taxed (i.e. you have a tax-free component, and your taxable component is taxed at your marginal tax rate, subject to a 15% rebate) between preservation age (currently 55) and age 60. After a member turns 60, the income is totally tax free.

TTR and salary sacrifice strategy can increase your overall retirement savings

Because the income that you draw from a TTR pension is concessionally taxed (if taxed at all), implementing a TTR and salary sacrifice strategy can allow you to reduce the amount of income tax you pay. Such a strategy involves salary sacrificing your wage into super up to your annual limits, while using your TTR pension to replace the lost income.

Because your TTR pension is concessionally taxed, you don’t have to draw as much income as you are salary sacrificing to maintain the same after-tax income. This strategy can significantly increase your overall savings towards retirement.

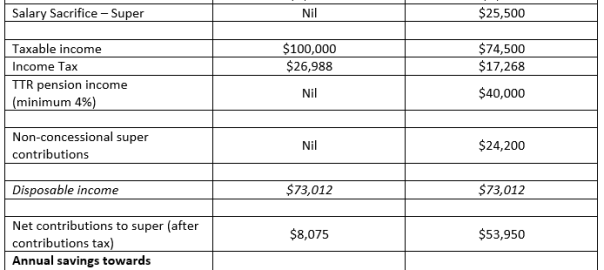

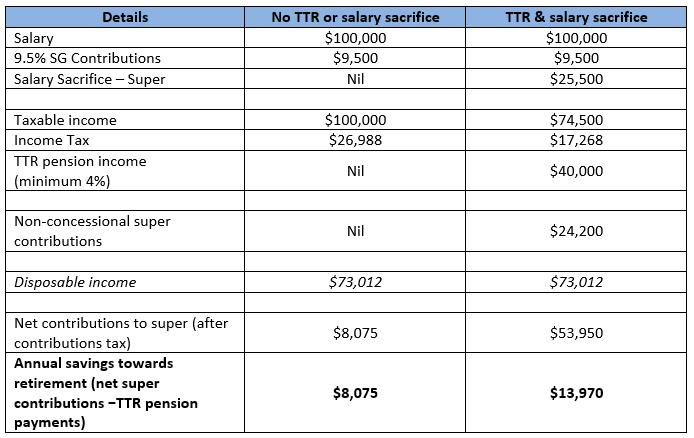

Example:

Let’s look at Michael. He is a 61-year-old engineer earning $100,000 per year, and he has $1,000,000 is his superannuation.

By making $24,200 worth of after-tax non-concessional contributions into superannuation, Michael maintains his annual disposable income, yet increases his savings towards retirement by $5,895 per annum. When this amount is combined with the potential tax savings of $9,000 per year presented by holding investments within a tax-free environment, this strategy is saving Michael approximately $15,000 per year in tax.

Three main factors to consider when starting a TTR pension

Ensure you meet your minimum annual TTR pension income

You must draw at least 4% of your TTR pension balance annually. The balance is calculated when the TTR pension starts and then recalculated on 1 July each year. However, as you can see in the example above, if you have made maximum salary sacrifice contributions, you can make non-concessional contributions up to your annual limit to ensure that your retirement pool continues to grow.

Ensure you don’t exceed your maximum annual TTR pension income

You must not draw more than 10% of your balance annually.

Ensure that your SMSF trust deed permits a TTR pension

If you have not updated your trust deed since 2005, it is extremely unlikely that it will allow for a TTR pension. Therefore, it is important to check you trust deed prior to implementing such a strategy.

If you have any questions about Transition to Retirement or Salary Sacrifice strategies, give the JBS team a call.