Non-Concessional Contribution Changes

In our last CPE article we talked about the recent changes the government has made to the previously proposed non-concessional contribution life-time cap of $500,000. To re-cap, the Government has back tracked on this proposal and has instead changed it to an annual cap of $100,000, with the ability to bring-forward 3 years’ worth of contributions from 1 July 2017. Your super balance must also be below $1.6 million to be able to make the contributions.

Since then the government has provided further direction on how the proposed bring forward rule and the $1.6 million cap will work.

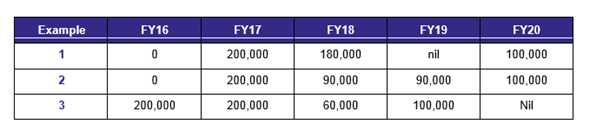

Under current rules you can make a total of $180,000 in one year or $540,000 if you bring-forward 3 years’ worth of contributions. If you as an individual have triggered the bring-forward rule in FY16 and FY17, but you have not used it fully by 30 June 2017, transitional rules will apply.

If you trigger the bring-forward provisions in FY17, the transitional cap will be $380,000 (which is the current $180,000 cap plus the new $100,000 annual cap for FY18 and FY19). If you triggered the bring-forward rule in FY16, the transitional cap is $460,000 (current annual cap of $180,000 for FY16 and FY17, plus the $100,000 for FY18).

The below table provides an example of how this may work in specific situations, with example one and two outlining how the $380,000 bring-forward cap may work, and example three highlighting how the $460,000 cap works with the example contributions:

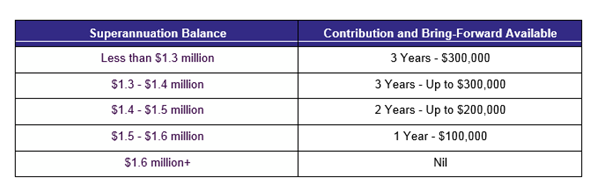

In relation to the $1.6 million eligibility threshold, you are unable to make further non-concessional contributions if your super account is above $1.6 million. Your balance will be determined as at the 30th of June in the previous financial year. If your balance is close to $1.6 million, you can only make a contribution or use the bring-forward rule to bring your balance up to $1.6 million without going over, this is summarised below.

As always these measures are not yet legislated and therefore could change yet again. The draft legislation is expected in the next few weeks.

If you have made any non-concessional contributions in the previous three financial years and are concerned how this may affect you and your future contributions, feel free to contact any of the team here at JBS.

paid out of their super either as a lump sum or income stream. Under the super laws, the deceased’s superannuation can’t remain in their super account and must be paid out as soon as practicable.

paid out of their super either as a lump sum or income stream. Under the super laws, the deceased’s superannuation can’t remain in their super account and must be paid out as soon as practicable.

on impulsive or unnecessary items

on impulsive or unnecessary items

insurance one we prefer to avoid however is necessary. Most Aussie families would find it difficult and almost impossible to meet daily living expenses should the main income earner pass away. This often leads to families having to move back in with relatives, increasing debt levels and even losing the family home.

insurance one we prefer to avoid however is necessary. Most Aussie families would find it difficult and almost impossible to meet daily living expenses should the main income earner pass away. This often leads to families having to move back in with relatives, increasing debt levels and even losing the family home.