Changes to Powers of Attorney

A Power of Attorney is a document that a person prepares to enable another person to make decisions on their behalf. On 1 September 2015 changes to Victorian power of attorney laws came into effect with the commencement of the Powers of Attorney Act 2015 (the Act).

Due to abuse of enduring powers of attorney, it was a necessary move to improve protection and to introduce a new supportive attorney appointment.

The new law sets out:

• The General Power of Attorney will be called general ‘Non-Enduring Power of Attorney.’

A Non-Enduring Power of Attorney will undergo only minor changes and remain largely governed by the previous statutory and common law provisions.

• The consolidation of the enduring power of attorney (financial) and power of guardianship into one enduring power of attorney.

This means that one form can now be used to manage a client’s financial and/or personal matters.

• A new definition of ‘decision-making capacity’ and provides guidance in relation to the factors that should be taken into account when assessing decision making capacity.

Though ‘capacity’ is a key concept when dealing with powers of attorney, there was no clear definition of what that actually meant in any of the existing laws. Following new mental health laws enacted in 2014, this law defines decision-making capacity and therefore shows that a person is presumed to have decision-making capacity unless there is evidence to the contrary.

• There will be a ‘Supportive Attorney’ role created. This allows a person to choose someone to support them to make and give effect to their own decisions such as banking and financial decisions.

The Act recognises that a person may have decision making capacity if they have practicable and appropriate support. The final decisions remain the decisions of the person and not the supportive attorney appointment. A person may have more than one support attorney appointment.

• The Act adds safeguards to increase the protection of people making an enduring power of attorney or supportive attorney appointment.

The Act has also clarified VCAT’s powers in relation to enduring powers of attorney and has created new indictable offences punishable by up to 5 years imprisonment or 600 penalty units. One penalty unit is currently worth $151.67.

Enduring powers of attorney (medical treatment) are not impacted by the changes and will continue to be regulated separately under the Medical Treatment Act. The new law does not invalidate existing powers of attorney.

Enduring powers of attorney (medical treatment) are not impacted by the changes and will continue to be regulated separately under the Medical Treatment Act. The new law does not invalidate existing powers of attorney.

The new Power of Attorney must be in writing and must be in the prescribed form. The form set out the minimum requirements for what to include in a form to make, revoke (cancel), resign or provide notification (where required) in relation to enduring powers of attorney and supportive attorney appointments under the new Act.

When considering making a Power of Attorney as a principal or if you are or are intending to act as an attorney, you should carefully consider the implications of the new laws.

Visit the Victorian Government Department of Justice and Regulation website for more information about the changes to power of attorney laws.

If you would like to discuss your estate planning requirements please give JBS a call.

This article is not intended to be legal advice and is not a substitute for legal advice.

ave to wait at least a month as well.

ave to wait at least a month as well.

nor private health insurance, yet when it comes to our health, there is no doubt you would want the best treatment available.

nor private health insurance, yet when it comes to our health, there is no doubt you would want the best treatment available.

ear, non-concessional contributions are limited to a maximum of $180,000. If aged 64 or under on 1 July 2014, you’re able to bring forward up to three years’ worth of contributions (up to $540,000) provided you haven’t done this previously.

ear, non-concessional contributions are limited to a maximum of $180,000. If aged 64 or under on 1 July 2014, you’re able to bring forward up to three years’ worth of contributions (up to $540,000) provided you haven’t done this previously.

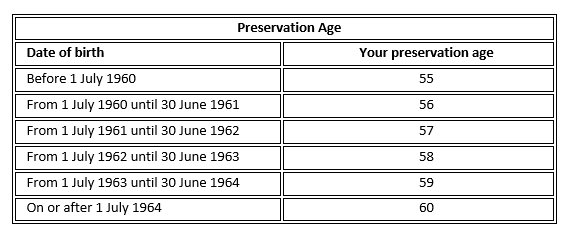

40?? Either way, you get to have a party, and get lots of presents. But one present that you won’t be able to get is your superannuation.

40?? Either way, you get to have a party, and get lots of presents. But one present that you won’t be able to get is your superannuation.