Pension Changes Means Reduced Tax Savings

Rule changes occur regularly with the Government in power tweaking legislation to make it fairer for all and ensure that the Government isn’t relied upon to fund everyone’s retirement through the Age Pension. This balancing act means that the strategy you implemented last year may no longer be beneficial for you or worse, not allowed. One change that is due to take effect from 1 July 2017 is the change of the tax treatment for Transition to Retirement pensions.

Transition to Retirement (TTR) pensions were introduced back in 2005 to allow those people that were easing into retirement by dropping their working hours to supplement their wages with an income from their super balance. However, while this was very useful for those in retirement transition, it also proved to be a powerful financial planning strategy, recycling funds through the super system to achieve the same take home pay however a reduced tax liability, meaning more funds are held in your superannuation account building for your eventual retirement. The Government and ATO knew of this strategy however as it was within the bounds of the laws in place, it has been accepted for use.

It does seem, however, that the Government now understands the additional tax that could be found and has implemented changes to take effect 1 July 2017 to make a TTR pension lose its tax-free status. This means that a TTR pension will have the same tax treatment as if it was in a superannuation account (15% tax rate). For those in the retirement transition space, it probably won’t change much as they need to subsidise their income and if the money wasn’t held in pension, it would be subject to the 15% super tax rate anyway. For those who have employed a TTR strategy to reduce tax, the tax savings will be reduced.

The strategy may still be beneficial, especially if you are able to achieve a significant salary sacrifice contribution from a higher income, however the tax savings will drop as the pension fund will now be subject to the 15% tax rate also.

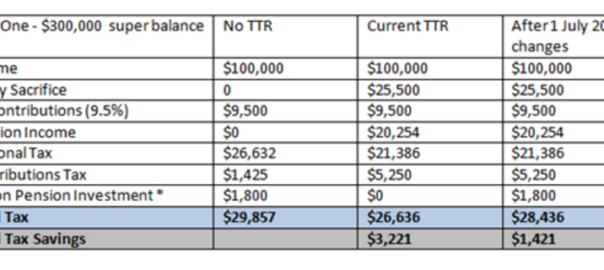

Example:

* For the purposes of this simplistic calculation, ‘Tax on Pension Investment’ is the 15% tax on investment income earned (4%) while money is held in a TTR pension. If assets were sold during the year, CGT would also be payable, making it again less tax effective. As this individual is under age 60, pension income is taxable.

Some clients situations allow them to maintain a tax-free pension or become eligible to establish one in the future. For this reason it is critical that all TTR strategies are reviewed prior to 30th of June 2017 as the new rules may not be applicable to you.

While you need to be making an appointment with your Financial Adviser to discuss the changes and determine if there’s still a benefit for you to continue with your TTR, more than anything this should highlight the need to have an ongoing relationship with a financial planner. Make sure you take up every opportunity to have a regular review of your financial plan, your objectives, determine if you are on track to reaching your goals and determine if the strategies in place are still appropriate. Your situation may not have changed but legislation may have.

I started gardening four years ago as a way of relaxing. What started as one small garden bed in the backyard quickly turned into me redesigning the entire front yard! My favourite time of year has to be end of winter through to spring. That is when all the bulbs that are hidden in the various garden beds come to life again and dazzle us with their colour.

I started gardening four years ago as a way of relaxing. What started as one small garden bed in the backyard quickly turned into me redesigning the entire front yard! My favourite time of year has to be end of winter through to spring. That is when all the bulbs that are hidden in the various garden beds come to life again and dazzle us with their colour. in the fridge for five weeks and then can be planted in May. It sounds odd, putting bulbs into the fridge before planting, but they need to be chilled in order to flower.

in the fridge for five weeks and then can be planted in May. It sounds odd, putting bulbs into the fridge before planting, but they need to be chilled in order to flower.

insurance one we prefer to avoid however is necessary. Most Aussie families would find it difficult and almost impossible to meet daily living expenses should the main income earner pass away. This often leads to families having to move back in with relatives, increasing debt levels and even losing the family home.

insurance one we prefer to avoid however is necessary. Most Aussie families would find it difficult and almost impossible to meet daily living expenses should the main income earner pass away. This often leads to families having to move back in with relatives, increasing debt levels and even losing the family home.

Enduring powers of attorney (medical treatment) are not impacted by the changes and will continue to be regulated separately under the Medical Treatment Act. The new law does not invalidate existing powers of attorney.

Enduring powers of attorney (medical treatment) are not impacted by the changes and will continue to be regulated separately under the Medical Treatment Act. The new law does not invalidate existing powers of attorney.

ave to wait at least a month as well.

ave to wait at least a month as well.

On the weekend of the Queen’s Birthday, I was lucky (or unlucky some might say) enough to spend the time repairing the fences around my family home. Kristyn and I had a few helping hands with my mum and dad coming down from Shepparton to help; my brother and sister in law were roped in too.

On the weekend of the Queen’s Birthday, I was lucky (or unlucky some might say) enough to spend the time repairing the fences around my family home. Kristyn and I had a few helping hands with my mum and dad coming down from Shepparton to help; my brother and sister in law were roped in too.