Reviewing Your Personal Insurance

At a time of mass media, there is an abundance of stories and ads about the importance of insurance cover. But what happens when you’ve had your cover put in place?

At a time of mass media, there is an abundance of stories and ads about the importance of insurance cover. But what happens when you’ve had your cover put in place?

With the pace of day to day life, there is a tendency for people to set and forget about their cover. However, it is imperative that your personal insurance policies are reviewed on a regular basis to ensure you’re adequately covered.

How do you know when it’s time to review your insurance policies?

There are several life stages and events, which should act as a trigger for you to review your insurance policies. Whether it be more responsibility such as starting a family, buying a house or even stressful events such as divorce or the death of a family member; these events should be treated as a call to action to review your insurance policies.

Starting a family and/or buying a family home

Whether you are having your first child or buying your first home these are memorable moments of your life; with these milestones comes the desire to protect the things that are most important to you. Personal insurance policies can often be complicated and may require lengthy amounts of time to put in force. It’s a good idea to review and implement adequate insurance cover before life’s adventures occur.

Death of family members

With it is the loss of a loved one or someone close to you taking ill, it is in moments like these we consider our own mortality and what we can do to prepare for life’s unexpected eventualities. Ask yourself, do I have adequate insurance in place if something was to happen to me?

Personal insurance cover should be reviewed but not limited to the following situations:

- Marriage or divorce

- Starting a family

- Buying a house

- New job

- Kids enrolling in a new school or completing their education

- Illness or death in the family

By being proactive you are fulfilling your wish to protect the people around you financially should something occur to you.

Case Study:

Jody is a 28-year-old working as a nurse and wants to provide funds to look after herself should something happen so she has implemented a Total & Permanent Disability (TPD) cover. This gives Jody peace of mind knowing that she has the cover the will support her in a difficult time.

Mark is a married 40-year old that needs to make sure income keeps coming in to provide for his living expenses if he can’t work. He worked with the JBS Financial team to assess his situation and has now implemented income protection cover. In our discussion with Mark, we discovered that Mark is a small business owner so not only is important to have the appropriate insurance in place to support his family but we also discussed Key Person insurance for the business.

Personal insurance is a complicated area and should be discussed with a financial adviser. Reach out to the JBS Financial team to review your circumstances and to ensure adequate insurance cover is in place for you.

There are 2 ways to structure jointly held assets and both are treated differently for estate purposes. The first and more common way is what is known as ‘Joint Tenants’. In this scenario, if you were to die, the asset automatically goes to the other owner. For example, a husband and wife purchase a house as joint tenants, if the husband were to die, the wife would now own the entire house. It does not form part of his Will.

There are 2 ways to structure jointly held assets and both are treated differently for estate purposes. The first and more common way is what is known as ‘Joint Tenants’. In this scenario, if you were to die, the asset automatically goes to the other owner. For example, a husband and wife purchase a house as joint tenants, if the husband were to die, the wife would now own the entire house. It does not form part of his Will.

If you have particular wishes, simply writing a name or ticking a box may not be sufficient to realise your intended plans. In many cases, the absence of correct estate planning documentation will see decisions made by the trustees of your super fund on where the funds will be allocated, potentially following generic rules which may see an undesired outcome.

If you have particular wishes, simply writing a name or ticking a box may not be sufficient to realise your intended plans. In many cases, the absence of correct estate planning documentation will see decisions made by the trustees of your super fund on where the funds will be allocated, potentially following generic rules which may see an undesired outcome.

If you are making either concessional or non-concessional contributions into your super fund, you will be able to apply to have your voluntary contributions, as well as associated earnings, released to help you purchase your first home. Since your concessional contributions are taxed at 15% as opposed to your marginal tax rate, the FHSS scheme can be an effective tool in helping you save for your first home.

If you are making either concessional or non-concessional contributions into your super fund, you will be able to apply to have your voluntary contributions, as well as associated earnings, released to help you purchase your first home. Since your concessional contributions are taxed at 15% as opposed to your marginal tax rate, the FHSS scheme can be an effective tool in helping you save for your first home.

Sell, Sell, Sell

Sell, Sell, Sell

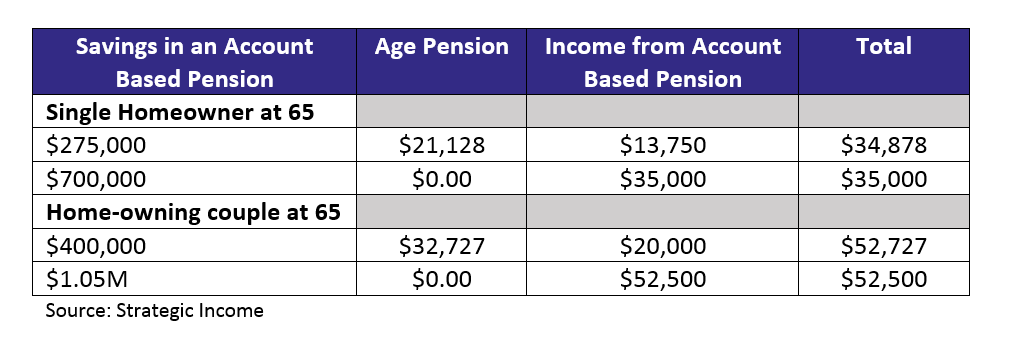

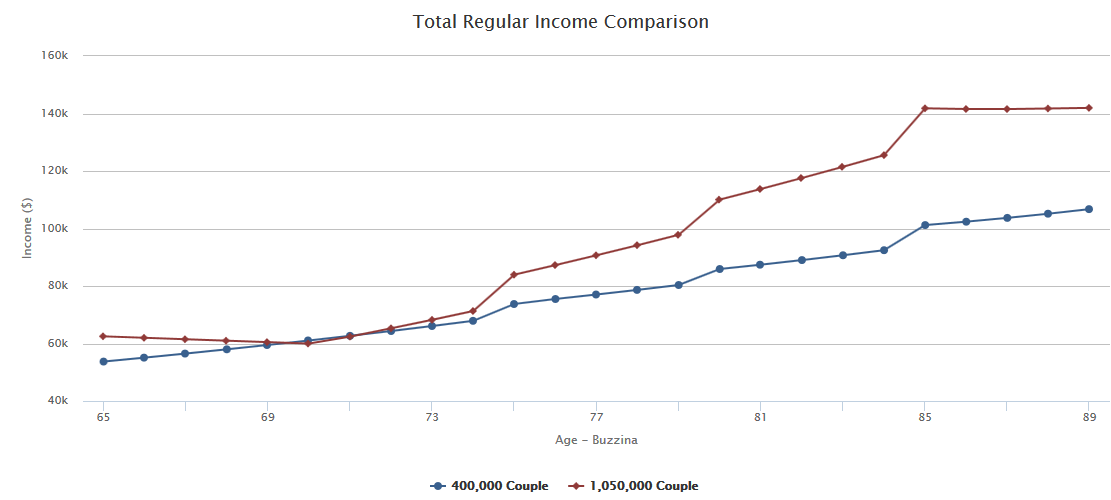

Being an adviser comes with a huge amount of responsibility, that we often take for granted and it’s not until we are able to sit back and reflect on all the good that we do that we often realise just how much of a difference we can and do make in our client’s lives. Take today, let me tell you about three clients, their stories and how it all unfolded, firstly let me introduce you John* and Sue*, they are both 70 and fairly typical retiree clients. They have combined investible assets of $850,000 and are receiving overseas pension income of $17,000. Their living expenses are around $60,000 including some low-cost holidays and they don’t qualify for any Centrelink at this point.

Being an adviser comes with a huge amount of responsibility, that we often take for granted and it’s not until we are able to sit back and reflect on all the good that we do that we often realise just how much of a difference we can and do make in our client’s lives. Take today, let me tell you about three clients, their stories and how it all unfolded, firstly let me introduce you John* and Sue*, they are both 70 and fairly typical retiree clients. They have combined investible assets of $850,000 and are receiving overseas pension income of $17,000. Their living expenses are around $60,000 including some low-cost holidays and they don’t qualify for any Centrelink at this point.

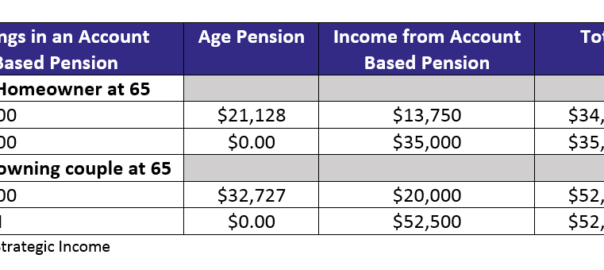

Unfortunately for some, the Age Pension will be critical to fund their retirement, but the Age Pension age doesn’t need to be your Retirement Age. There’s a few things you can do to help reduce your reliance on the Age Pension and retire when you want to retire, our motto is that we’d rather you be working because you want to, not because you have to.

Unfortunately for some, the Age Pension will be critical to fund their retirement, but the Age Pension age doesn’t need to be your Retirement Age. There’s a few things you can do to help reduce your reliance on the Age Pension and retire when you want to retire, our motto is that we’d rather you be working because you want to, not because you have to.