Is Your Insurance About To Be Cancelled? – Urgent Action Required

In February this year, the Government passed legislation which prevents some Superannuation funds providing insurance to members with inactive superannuation accounts, unless a member has directed otherwise.

It is a common practice for many individuals to have multiple Superannuation Funds for insurance purposes.

This may be done for two key reasons:

- To access insurance policies provided through large superannuation funds which are often cheaper.

- To keep legacy insurance policies which may offer better benefits or lower premiums than new policies, especially for older members.

In these circumstances, it will often be the case that one Superannuation fund receives ongoing Superannuation Contributions while the other account simply holds a nominal balance to ensure that the insurance is maintained.

In these circumstances, it will often be the case that one Superannuation fund receives ongoing Superannuation Contributions while the other account simply holds a nominal balance to ensure that the insurance is maintained.

Under the new legislation, you now may lose your insurance cover if one of your Superannuation funds is considered inactive because it has not received a contribution or a rollover for a continuous period of 16 months.

At 1 July 2019, if any of your Super funds are considered inactive for 16 months your insurance will be terminated.

We are concerned that insurance will be unknowingly closed for these accounts because members have not checked their correspondence, especially for those who rely on this insurance held separately.

This could have a devastating impact on policy holders or their beneficiaries if their insurance cover was unknowingly terminated. Furthermore, it may be extremely difficulty or costly to try and access insurance at a later stage of life.

Here is the link to more information.

So what can you do?

You may have received an email or letter over the past couple of weeks. It is important that if you wish to maintain your insurance cover that you take necessary steps as soon as possible. This includes either:

- Providing a direction to your Superannuation fund that you wish to ‘opt-in’ for your insurance cover to be maintained.

- Making a contribution or rollover to your ‘inactive’ Superannuation fund so that the period for which your fund starts to be inactive is reset. However, we stressed that you should also ‘opt-in’.

How can we help?

If you are concerned you are going to be affected by these changes or need assistance with your insurance, please feel free to contact the JBS Financial team to arrange a time to meet so that we can discuss your particular requirements in more detail. We urge you to not leave reviewing your situation till the last minute. You can contact us here.

Direct Life Insurance is defined as being sold to consumers by insurers or their sales partners, by outbound telemarketing, inbound phone calls from consumers, online or face to face (through bank branches). These products are sold with general advice or no advice given meaning that the consumer’s circumstances are not taken into account.

Direct Life Insurance is defined as being sold to consumers by insurers or their sales partners, by outbound telemarketing, inbound phone calls from consumers, online or face to face (through bank branches). These products are sold with general advice or no advice given meaning that the consumer’s circumstances are not taken into account.

When we’re young and free with the world at our feet, we think that we’re pretty indestructible (I remember that time). Life’s all about fun! Travel, drinking, friends… who wants to think about grown up things like insurance? While we might not want to think about it, it doesn’t stop that fact that we all need it.

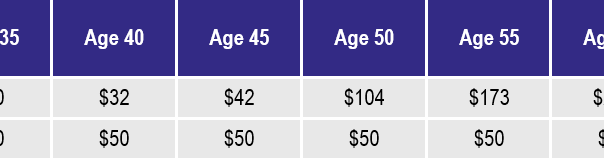

When we’re young and free with the world at our feet, we think that we’re pretty indestructible (I remember that time). Life’s all about fun! Travel, drinking, friends… who wants to think about grown up things like insurance? While we might not want to think about it, it doesn’t stop that fact that we all need it. Also, taking out insurance while you’re young can save you thousands in the long run. While you’re young, you’re relatively healthy and therefore taking out insurance is cheaper. You are more likely to get standard rates, which means that you are no more of a risk of claiming than anyone else your age, unlike when you’re older, rounder and doing less exercise. If you can get standard rates at a young age, you can take out level premiums. This means that you can spread the risk of claiming over the life of the policy rather than just year by year and save a heap in the long run!

Also, taking out insurance while you’re young can save you thousands in the long run. While you’re young, you’re relatively healthy and therefore taking out insurance is cheaper. You are more likely to get standard rates, which means that you are no more of a risk of claiming than anyone else your age, unlike when you’re older, rounder and doing less exercise. If you can get standard rates at a young age, you can take out level premiums. This means that you can spread the risk of claiming over the life of the policy rather than just year by year and save a heap in the long run!