Longevity Risk in Super

As the baby boomers of Australia are now entering retirement, the topic of longevity risk within superannuation has become increasingly important. The longevity risk of superannuation refers to the risk of retirees running out of money in their super account before they die.

Contrary to the common thought of Aussies using up their entire super benefits earlier on, close to 50% of retirees draw down the minimum amounts from their super accounts, in an attempt to protect themselves against longevity risk. Whilst there are still a portion of retirees drawing down unsustainable amounts from their retirement benefits each year, it’s crucial to get the right balance in order to have a comfortable retirement. Furthermore understanding and managing the longevity risks in super can be the difference between having enough in retirement and running short.

There are 3 components of longevity risk which are;

Mortality Risk – This risk is associated with the chance of death along a certain time frame. With medical and technological advancements, the average life span of Aussies continue to increase each year, which means our super benefits need to also last that extra distance.

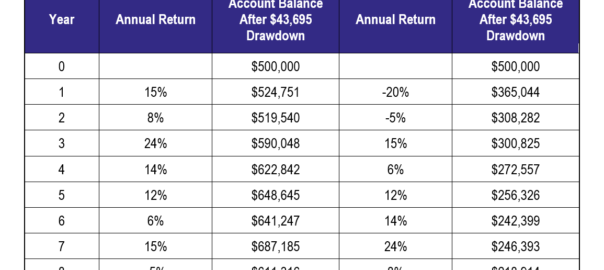

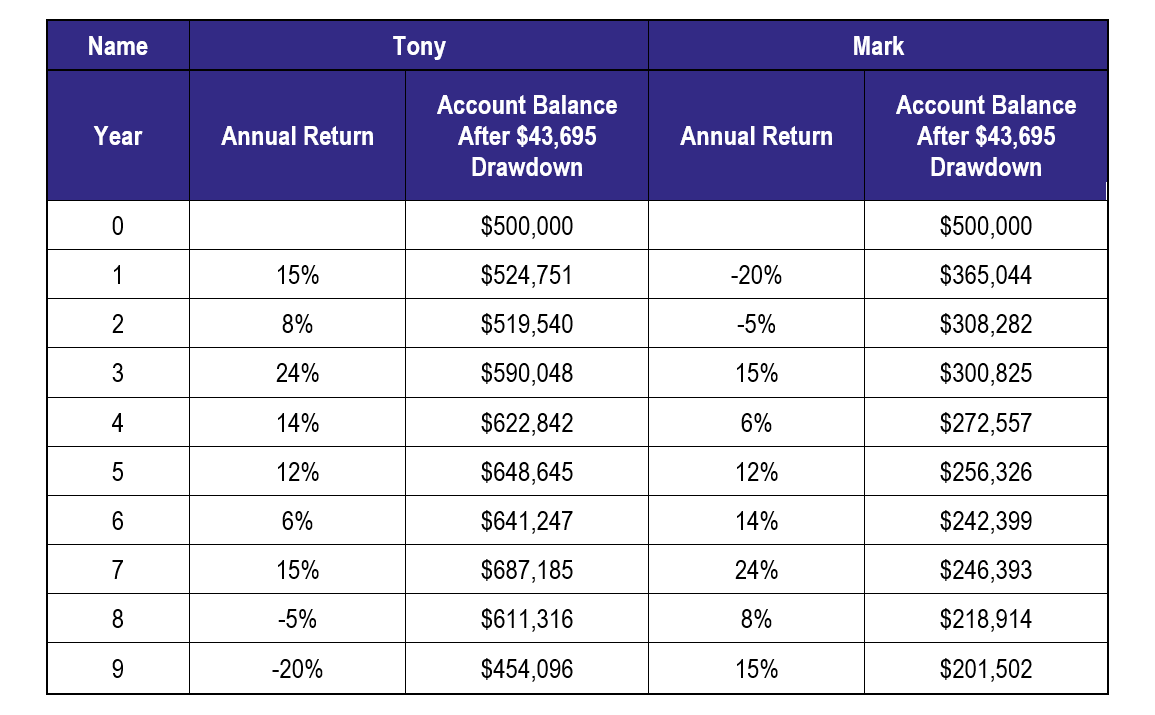

Volatility and Sequencing Risks – Volatility risk relates to the chance of suffering losses in our super funds due to volatility in the financial markets. Whilst sequencing risk is associated with the order of returns, which results in the retiree with less money due to losses suffered in the initial stages of retirement. Take for example the following table, which shows Tony and Mark, both starting off their retirement with $500,000 in super and drawing an annual income for $43,695 per annum (Association of Superannuaton Funds of Australia’s standard for comfortable retirement), from their retirement benefits.

As shown in the above table, over a 9 year period with an average return of 8%, we can see Tony is in a better position as his super fund performed really well early on in his retirement. Whereas Mark suffered poor performance early on in his retirement, which affects the balance of his retirements benefits in future years.

Expenses Risk – This risk is associated with the expenses depleting retirees super benefits early on in their retirement. Aside from the travelling and discretionary spending one type of expense that is commonly missed is medical and personal care expenses. Tied to morality risk, being able to live longer with the help of modern medicine and technology often doesn’t come cheap or free. As such taking into account medical and carer expenses, is crucial.

Ensuring sufficient super benefits in retirement can be very daunting, especially considering all the risks associated with longevity. There are however professionals such as financial advisers, who can assist in making the journey much smoother. Aside from being able to assist clients in reaching their retirement goals, an adviser can also help in determining an optimal amount to withdraw from super each year so their clients get a well-balanced retirement life.

– Andy Lay –