So What’s in a Loan?

Offset vs Redraw

When it comes to choosing a home loan, we often simply choose the one with the lowest interest rate. However one thing we should take into account is whether the loan has an option to add an offset account or not.

What is an offset account?

An offset account is a bank account attached to a loan that ‘offsets’ the loan balance. It does not earn any interest but instead reduces the interest payable on the loan.

For example, if you have a $300,000 loan with an interest rate of 4%. The interest payable on the loan is $12,000. If however you had an offset account with a balance of $50,000. The interest payable is calculated on a balance of $250,000 ($300,000 less $50,000) so $10,000.

Note that if instead you paid this $50,000 into the loan then the total loan would also be $250,000 and the interest payable would also be $10,000. The advantage of having an offset however is that the $50,000 is in a bank account and therefore can be withdrawn very easily.

Why not just pay money into the loan and then use a redraw facility?

Having a redraw facility on your loan gives you the option to redraw the extra money you’ve paid into the loan giving you the same flexibility as having an offset account. There is however 1 key difference. When utilising the redraw facility, you are paying down the loan and redrawing whereas with an offset account, you aren’t actually paying down this loan.

So why does this matter? Tax law dictates that the tax deductibility of a loan is determined by its purpose. So if the purpose of the loan was to purchase an income producing asset, then the interest becomes tax deductible. If the purpose of the loan is to go on holiday, the interest is not tax deductible. This is where an offset account shines.

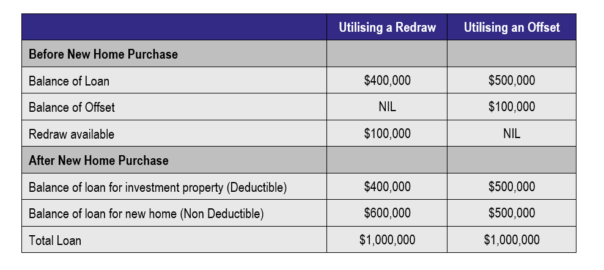

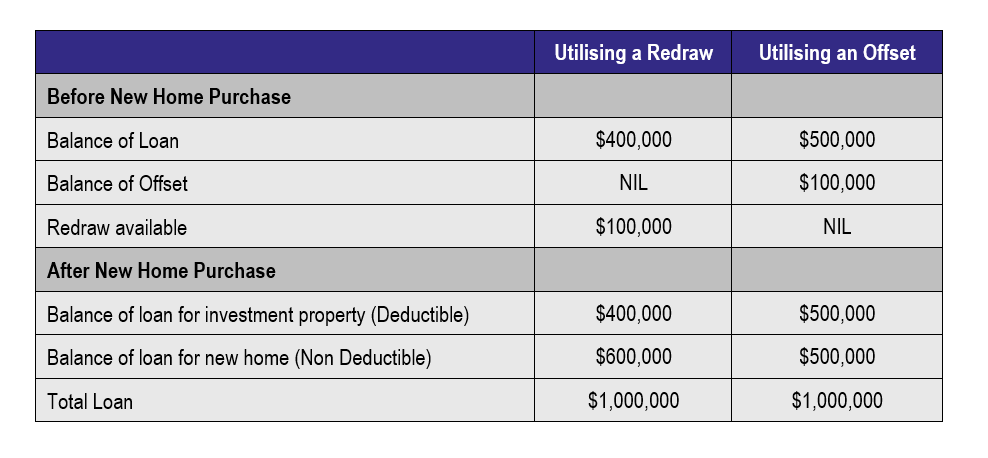

For example, let’s take a $500,000 loan which was initially purchased to buy a home. 10 years down the track, you’ve paid off $100,000 so the loan is now $400,000. You redraw that $100,000 to purchase a new home and borrow an additional $500,000, with the plan to turn your existing home into an investment property.

In this scenario while the initial borrowing amount was $500,000 once you’ve paid it down, only $400,000 is being used to fund the now investment property and is hence tax deductible.

In a separate scenario, you utilise an offset account. You have a current loan of $500,000 with an offset account of $100,000. You then withdraw the $100,000 from the offset account and borrow an additional $500,000 to purchase a new home. In this example the loan for the new home is $500,000 instead of $600,000 however the loan on the investment property is $500,000 instead of $400,000.

By utilising an offset account, even though your total loans are the same, your tax deductible loan is $100,000 more which will provide you with more tax deductions (and hence less tax payable) than if you used the redraw facility.

What are the pitfalls?

An offset account is a bank account and can be easily accessed. This is the offset accounts greatest weakness. If you are the kind of person that struggles to save money or can be tempted by large bank account balances you may find yourself using the offset money to purchase a new car, go on holidays etc. as you will have large cash amounts easily available to you. In contrast, a redraw facility adds that extra step which may stop you from accessing those extra mortgage payments. So while you are thinking you are paying down the loan quickly using an offset account, yes you are reducing the interest payable, however the loan is not getting paid as fast as you may think as you continue to redraw the funds for personal spending.

Selecting a loan

Interest rates aren’t the only thing we need to consider when selecting a loan. We often need to consider the features of the loan. However, features aren’t everything, and they may be features that we do not need and a cheaper loan may be better suited. It is always advantageous to speak to an expert, where they can determine your needs and recommend a product that best suits. An offset account is only one feature. There may be other features that better suit your circumstances or a simple loan with the lowest interest rate may be the best.

If you would like to speak to a loan expert to make sure your loan is the best one suited to you, please call us on 03 8677 0688 and we will happily refer you to an expert.