Travel or tinned beans?

Which choice would you make? And believe it or not, at this age, with time on your side, getting ahead financially is easier than you think. If you are one who would choose travel over tinned beans, here’s three simple steps you can take now to set yourself up financially in the future – and skip the beans.

TIP 1: Set Financial Goals

TIP 1: Set Financial Goals

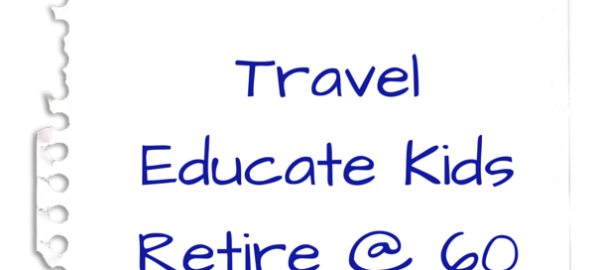

Start with a bucket list, what are all the things you’d like to do throughout your life? Now sort them into timeframes. Pick one core goal per timeframe and each pay slip you receive, allocate money toward that goal. For example:

– SHORT TERM (1-3 YEAR) GOAL: Go to New York for two weeks. Set up a savings account, contribute some every pay cheque.

– MID TERM (7-15 YEAR) GOAL: Educate your children. Consider an investment such as an investment property, managed fund or share portfolio, contribute even a small amount from every pay cheque.

– LONG TERM (20+ YEAR) GOAL: Have the choice to retire at 60. Make sure that your superannuation plan is the right one for you, considering fees, investment options, insurance coverage, and any other benefits. To have the ability to retire early, you might want to consider contributing funds to super above the legally required minimum amount (SG contributions) from your employer.

TIP 2: Pay Off Personal Debt

Paying interest is lost money. For example: If you have $3,500 owing on your credit card, paying 21.5% interest and are only making the minimum repayments of $70 a month – it will take you 90 years and 1 month to pay off and you’ll have racked up $27,050 in interest! Even by paying a little extra each month, say $150. You’ll repay it in two years 8 months and only accrue $1,074 interest. Earn more, spend less or use savings to get rid of credit card debt ASAP so you can start focusing on your exciting goals ahead.

TIP 3: Choose Super Investing Options Wisely

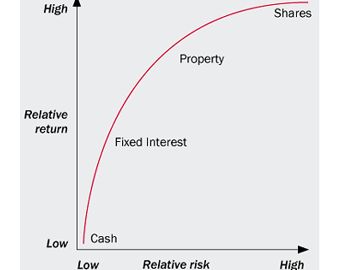

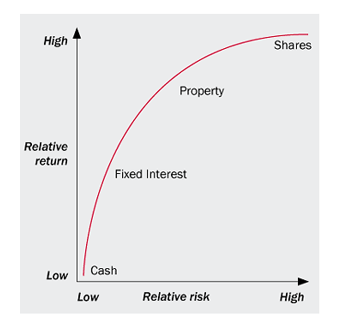

You can choose how you invest and contribute to your super. Compound interest 101: Say you’re 25 years old and you can access your super when you’re 65 years of age. If you have $1,000 in your fund currently and are earning $65,000 a year, contributing 9.5% of your annual salary, being $6,175. If you receive 5% returns, you’ll retire on $752, 979. If you receive 6% returns you’ll retire on $965, 941. If you receive 7% returns you’ll retire on approximately $1,250,000. We can’t change the timeframe with super but we can influence our rate of return. Always check what your agreed risk profile is. Whether you’re in a conservative (more cash, less shares, property) or high growth (less cash, more shares, property) investing option, it’s important to understand what assets make up your account and whether they will deliver the growth and income you require to meet your goals. But also remember that with greater potenital for growth is greater potential for loss so adjust your portfolio wisely based on your views.

You also have options to contribute on top of the legal minimum paid by your employer, contributing $1,000 per annum on top of employer contributions could result in as much as a $100,000 difference when you retire.

If you need help setting a spending and savings plan, reducing debt or would like more information around the investment options in your super, please contact our office today.

We can often also have goals wandering around in our mind that we end up forgetting so “ink it, don’t think it”. By writing down your dream or goal, you make a conscious commitment that this is what you want to achieve. Once you have made this commitment, put it in places that can easily be seen. Put it on your home screen of your phone, tablet or computer, your bathroom mirror, in your gym bag or on your kitchen fridge. These reminders and a positive mindset will help you stay motivated for achieving your goals.

We can often also have goals wandering around in our mind that we end up forgetting so “ink it, don’t think it”. By writing down your dream or goal, you make a conscious commitment that this is what you want to achieve. Once you have made this commitment, put it in places that can easily be seen. Put it on your home screen of your phone, tablet or computer, your bathroom mirror, in your gym bag or on your kitchen fridge. These reminders and a positive mindset will help you stay motivated for achieving your goals.