Superannuation, it’s a bit of mine field when it comes to knowing how to maximise your super contributions. But don’t worry, we’ll break it down for you:

Maximise concessional superannuation contributions

Concessional superannuation contributions for the 2014/15 financial year are limited to $30,000. However, if you were aged 49 or older on 1 July 2014, a transitional limit of $35,000 applies giving you the opportunity to maximise your concessional contributions before the end of the current financial year.

Claiming a tax deduction for personal superannuation contributions

If you’re intending to claim a tax deduction for personal superannuation contributions, a “Notice of Intention to Claim a Tax Deduction” (s.290-170 Notice) must be lodged with your superannuation fund before any one of the following events occurs, whichever is first:

– lodgement of the income tax return for the financial year in which the tax deduction is being claimed

– commencing a pension

– withdrawing superannuation benefits

– rolling over your superannuation to another superannuation fund

Maximise non-concessional contributions

Non-concessional contributions are personal contributions made from after-tax income. For the 2014/15 financial y ear, non-concessional contributions are limited to a maximum of $180,000. If aged 64 or under on 1 July 2014, you’re able to bring forward up to three years’ worth of contributions (up to $540,000) provided you haven’t done this previously.

ear, non-concessional contributions are limited to a maximum of $180,000. If aged 64 or under on 1 July 2014, you’re able to bring forward up to three years’ worth of contributions (up to $540,000) provided you haven’t done this previously.

Making large non-concessional contributions is a big decision and advice from a financial planner is recommended before any contribution is made.

Salary sacrificed contributions

Foregoing part of your salary in favour of having additional concessional contributions made to super by an employer may deliver tax advantages.

Existing salary sacrifice arrangements should be reviewed on a regular basis, at least annually. Reviewing a salary sacrifice arrangement before the end of the financial year and amending for the following financial year represents good planning.

Your superannuation contributions at 65

If you’re aged 65-74, your superannuation fund is only able to accept contributions if you have been gainfully employed or self-employed for a minimum period of 40 hours, worked over not more than 30 consecutive days, in the financial year in which the contribution is being made.

If you’re approaching 65 and not working, consider making superannuation contributions before your 65th birthday.

Government co-contributions for low income earners

If you earn less than $49,488 a year and make a non-concessional contribution to superannuation you may be eligible to receive a Government contribution of up to an additional $500. The actual amount, and eligibility for the co-contribution, depends on a number of factors including the proportion of total income derived from employment, age and taxable income.

Spouse contributions

Where you make a non-concessional contribution to superannuation for your spouse, you may be entitled to receive a tax offset of up to $540 if your spouse has an income of less than $10,800. The tax offset reduces if your spouse’s income is between $10,800 and $13,800. You will not receive a tax offset if your spouse’s income exceeds $13,800. The maximum offset available is 18% of the contribution made, subject to a maximum offset of $540.

Spouse contribution splitting

Superannuation laws allow for a person to split their concessional contributions with an eligible spouse to build up retirement savings for the other. Up to 85% of concessional contributions made in the 2013/14 financial year may be split with a spouse prior to 1 July 2015. Splitting superannuation contributions allows for couples to balance their superannuation savings between partners.

Life insurance held in super

On 1 July 2014, restrictions came into effect in relation to the types of insurance held through superannuation.

The new restrictions affect insurance policies that provide for the payment for an insured event that is aligned to a superannuation condition of release. In essence, the only new policies that can be taken out through superannuation after 1 July 2014 are those covering the following events:

– death

– terminal illness

– total and permanent incapacity – any occupation

– temporary incapacity

The new restrictions mean that you will no longer be able to take out a policy with your superannuation fund that covers trauma insurance, total and permanent disablement – any occupation and income protection insurance that provides ancillary (such as rehabilitation) benefits in addition to income replacement. Policies taken out prior to 1 July 2014 will not be affected by these new restrictions.

I started gardening four years ago as a way of relaxing. What started as one small garden bed in the backyard quickly turned into me redesigning the entire front yard! My favourite time of year has to be end of winter through to spring. That is when all the bulbs that are hidden in the various garden beds come to life again and dazzle us with their colour.

I started gardening four years ago as a way of relaxing. What started as one small garden bed in the backyard quickly turned into me redesigning the entire front yard! My favourite time of year has to be end of winter through to spring. That is when all the bulbs that are hidden in the various garden beds come to life again and dazzle us with their colour. in the fridge for five weeks and then can be planted in May. It sounds odd, putting bulbs into the fridge before planting, but they need to be chilled in order to flower.

in the fridge for five weeks and then can be planted in May. It sounds odd, putting bulbs into the fridge before planting, but they need to be chilled in order to flower.

ave to wait at least a month as well.

ave to wait at least a month as well.

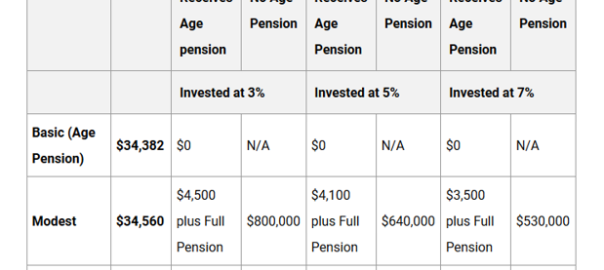

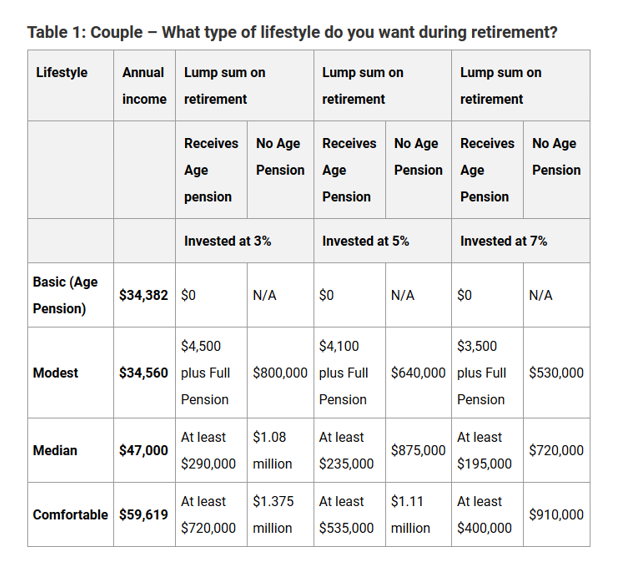

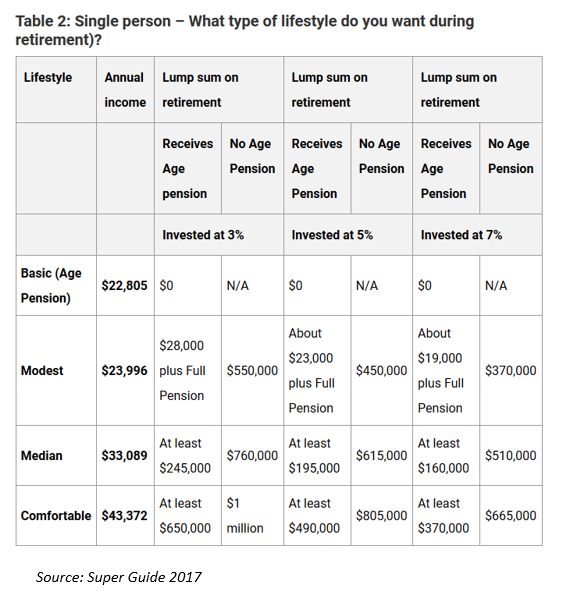

A vital element of retirement involves choosing how to use your super savings. To set yourself up for retirement and providing your future income, you will need to make decisions regarding how you are going to invest your funds, when it will begin, how much you wish to receive and how often you will need to receive payments.

A vital element of retirement involves choosing how to use your super savings. To set yourself up for retirement and providing your future income, you will need to make decisions regarding how you are going to invest your funds, when it will begin, how much you wish to receive and how often you will need to receive payments.