5 Unexpected facts about retirement

Most of us can only dream about leaving our work forever to do as we please. For those who are close to retirement however, this can be a time of excitement and relaxation. Spending countless days at the golf course or with our community groups, families and friends sounds like heaven on earth. The transition from full time work to full time play however may have some unforeseen pitfalls. Here are 5 facts about retirement that you should consider before retiring.

Time

One of the first things retirees quickly discover is that they have too much time on their hands with nothing to do. Playing a round of golf with mates or enjoying a drink at the bar will only fill up a certain amount of time in the day and you can’t go doing the same thing every day. Retired couples and singles alike will quickly become very unhappy once they run out of things to do.

One of the first things retirees quickly discover is that they have too much time on their hands with nothing to do. Playing a round of golf with mates or enjoying a drink at the bar will only fill up a certain amount of time in the day and you can’t go doing the same thing every day. Retired couples and singles alike will quickly become very unhappy once they run out of things to do.

Having ideas in your head about what to do in retirement is one thing; however actually doing them is another. Some experts are suggesting retirees have a day to day plan on what they want to do and even seek an adviser leading up to retirement. You will never be as busy as you were pre-retirement so it’s important to map out ongoing hobbies, part time work and social events before embarking on retirement.

Retired husband syndrome

Many couples get very excited about retiring together, travelling the world together and spending a lot of time together. If this is you then consider the fact that you and your other half may have been together for the past 30 years working full time. Aside from weekends and holidays, you never have to see each other for more than a couple of hours in the morning and night. Now all of a sudden you see each other 24 / 7 and may even start to discover that you can’t stand being together for a prolonged period of time. Determining your own hobbies, goals and friends will assist to avoid “retired husband syndrome’. Again, seeking help from an adviser may also assist in preparing you and your loving partner for retirement.

Not having enough money to fund retirement

Once retired you might have the goal to travel, see the world and complete your bucket list, unfortunately you might not have the funds to do so. Travelling can become very costly. A single international trip can set you back several thousand dollars if not more. By the time your second trip comes around you may find that your retirement funds are not adequate and you’ll need to start tightening the belt. Having a good financial planner early on can prepare you and set realistic goals for your retirement. This way you will have a clear expectation of what you can afford in retirement and prevent any nasty surprises once you’ve retired.

Entitlement to social security

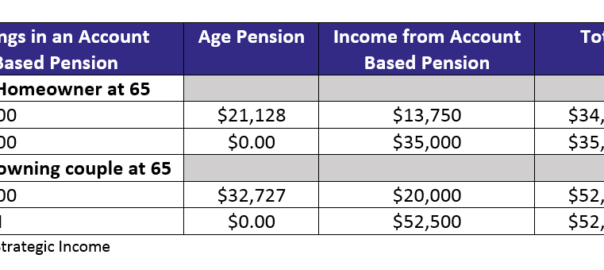

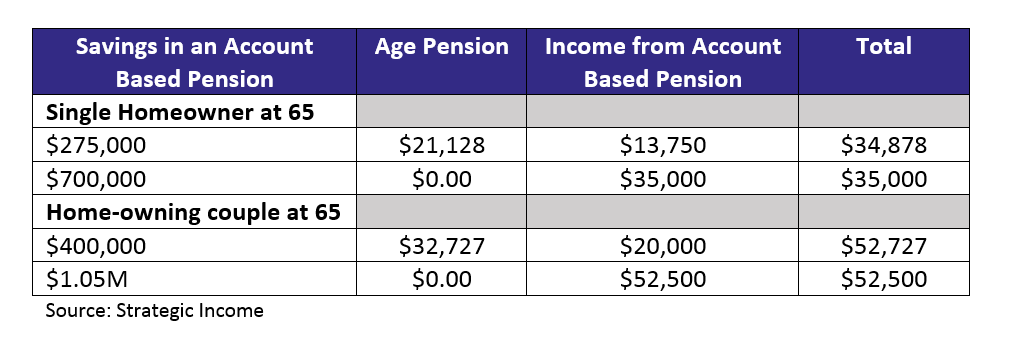

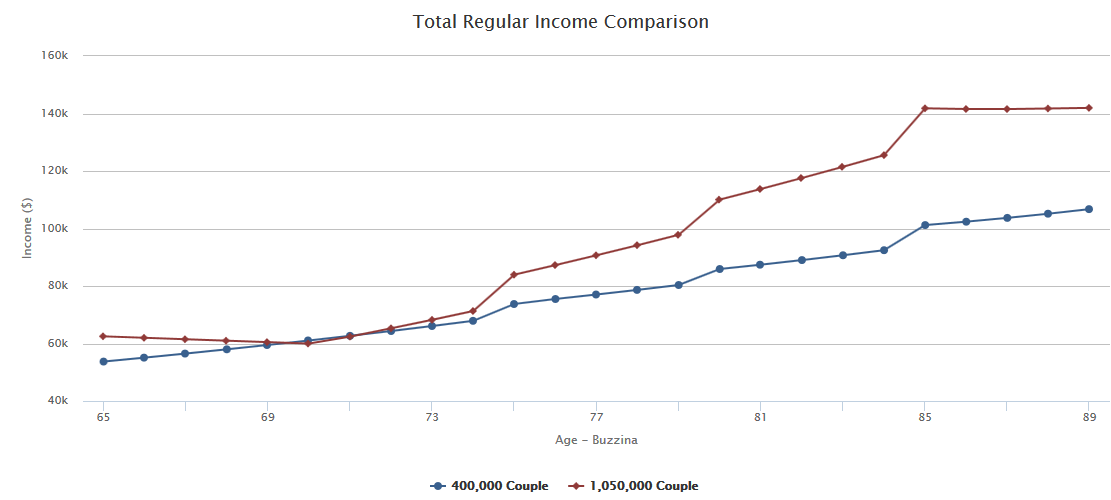

At the moment the Australian pension age is age 65.5 and increasing with each year. During retirement some retirees aren’t aware of what social security benefits they’re entitled to. Even if you are receiving funds from your Superannuation benefits, you may still be entitled to a government age pension (subject to the income and asset tests). Having a good financial adviser by your side will ensure you’re kept up to date regarding any social security payments you’re entitled to.

Losing your identity from not being at work

For those of us who are passionate about our profession, this becomes our identity. Anytime your friends or family think of Engineer, Accountant or Doctor, they think of you. So it’s no surprise that once you retire you may feel like you’ve lost your identity, which may lead to discontent and even depression. Without the daily interaction of your work colleagues your mental and even physical health may start to deteriorate. Retirees who are not very active tend to decline rather quickly mentally and physically. Joining up to the local gym, taking up classes and just continuing to meet new people will have a longer lasting effect for you.

Financial independence gives you the freedom to make your own choices, speak to the team at JBS to start your retirement journey today.

Unfortunately for some, the Age Pension will be critical to fund their retirement, but the Age Pension age doesn’t need to be your Retirement Age. There’s a few things you can do to help reduce your reliance on the Age Pension and retire when you want to retire, our motto is that we’d rather you be working because you want to, not because you have to.

Unfortunately for some, the Age Pension will be critical to fund their retirement, but the Age Pension age doesn’t need to be your Retirement Age. There’s a few things you can do to help reduce your reliance on the Age Pension and retire when you want to retire, our motto is that we’d rather you be working because you want to, not because you have to.

Since July 1 2017, the ten percent employment rule regarding tax-deductible super contributions has been replaced. The rule meant that a person could not claim a tax deduction on personal Super Contributions if more than ten percent of their assessable income was obtained as an employee. The new rule is now any person under age 65 now may be able to claim a tax deduction on their contributions regardless of their employment arrangement, whilst those aged between 65 and 74 need to satisfy the Work Test in order to be eligible to make a contribution, and subsequently claim a tax deduction.

Since July 1 2017, the ten percent employment rule regarding tax-deductible super contributions has been replaced. The rule meant that a person could not claim a tax deduction on personal Super Contributions if more than ten percent of their assessable income was obtained as an employee. The new rule is now any person under age 65 now may be able to claim a tax deduction on their contributions regardless of their employment arrangement, whilst those aged between 65 and 74 need to satisfy the Work Test in order to be eligible to make a contribution, and subsequently claim a tax deduction.

With all the festivities and celebrations over and done with, for most of us it’s now time to pick up the pieces and start the New Year a fresh, which is a perfect time to review your personal insurance needs. Research from one of Australia’s largest personal insurance companies have found that only 37% of Aussies aged between 18-69 actually have life insurance and even more disturbingly only 18% have disability cover and income protection insurance. Further findings include how Australians are grossly underinsured. It’s estimated that the underinsurance gap in Australia is approximately $1.8 Billion, meaning there are a lot of Aussies out there who believe they have sufficient insurance cover, but in fact don’t. For most of us, we don’t like to think about insurance and when asked about how much we have, the first response is usually “I don’t know”.

With all the festivities and celebrations over and done with, for most of us it’s now time to pick up the pieces and start the New Year a fresh, which is a perfect time to review your personal insurance needs. Research from one of Australia’s largest personal insurance companies have found that only 37% of Aussies aged between 18-69 actually have life insurance and even more disturbingly only 18% have disability cover and income protection insurance. Further findings include how Australians are grossly underinsured. It’s estimated that the underinsurance gap in Australia is approximately $1.8 Billion, meaning there are a lot of Aussies out there who believe they have sufficient insurance cover, but in fact don’t. For most of us, we don’t like to think about insurance and when asked about how much we have, the first response is usually “I don’t know”.