Protecting Our Future Plans

Planning for the future is essential to financial planning. Having money now is great but it’s having money 5, 10, 15 years from now that really counts when it comes to financial planning.

So a plan is developed using appropriate strategies providing you with money in the future enabling you to achieve your goals. However, what if things go wrong? What if something happens where you are not able to achieve your future goals? No, I’m not talking about investment returns.

When planning and saving for the future, your income, expense and savings levels are critical. They are the main things that will determine how much money you will have in the future. So what happens if your income all of sudden stops? Or if you have a large one off expenses that depletes your savings and may even put you into debt?

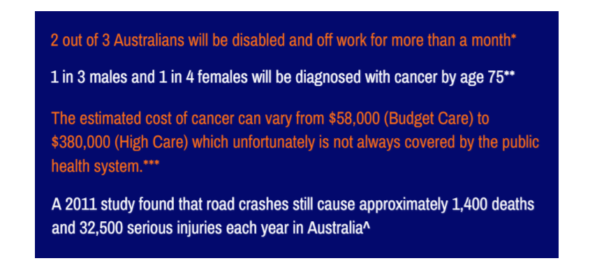

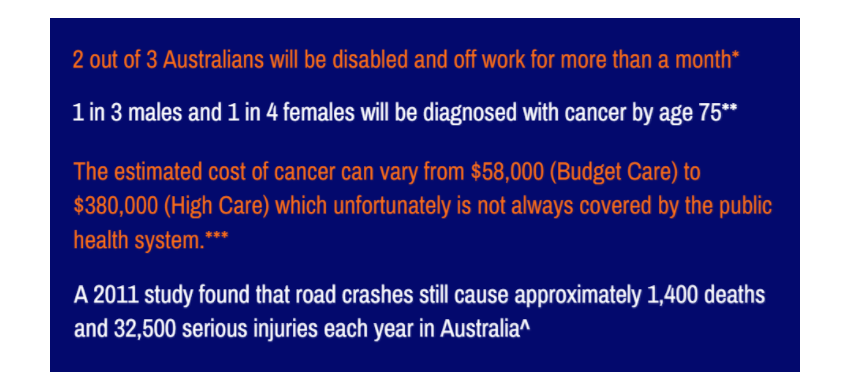

Did you know:

Potential injuries, illnesses and even death can significantly hinder our ability to reach our goals and may even make them impossible. Our human thinking of “It will never happen to me” just doesn’t cut it when you look at the above stats. Accidents happen and cancer does not discriminate but there is something that we can do to minimise the impact. Life Insurance.

There are 4 kinds of Life Insurance each providing cover under different circumstances:

Death Cover – As the name suggests, this provides a lump sum amount to your beneficiaries when you die.

Total & Permanent Disability (TPD) Insurance – As the statistics show, we don’t always die but we can have serious injuries that stop us from working. TPD cover provides a lump sum payment if we are permanently unable to work due to illness or injury such as what may happen if for example we are in a serious car accident.

Income Protection – This provides you with a regular income if you are unable to work due to illness or injury.

Trauma insurance – Also known as critical illness insurance provides you with a lump sum if you suffer a critical illness for example cancer or a heart attack. The lump sum can be used to help fund medical expenses, payout your loans or whatever it is that you require at that time.

Planning for the future is important but those plans can go straight out the window if something devastating like a serious health issue happen to us. While we cannot protect against the emotional, mental and physical consequences of something happening we can protect against the financial aspects using a combination of insurance policies protecting us against death, illness and injury. Insurance however is complicated and there are differences between the policies offered by insurers. To ensure that you not only have the correct amounts of insurance in place but also the right insurance policy for you please contact the JBS office on 03 8677 0688.

*2002 Report of the Disability Committee, IAA

**AIHW (2008) Cancer in Australia: an overview 2008

***Access Economics Pty Limited (April 2007) Cost of Cancer in NSW, Report for The Cancer Council NSW.

^’National Road Safety Strategy 2011-2020’ – Australian Transport Council, May 2011

– Liam Rutty –

We are a generation that was either studying or entered the workforce during the financial crisis which triggered a shift towards prioritising quality of life, experiences and adventure over money. I can’t count the number of times I have been tempted to try out a new restaurant with a fancy ambience or taking a short trip over the weekend just because I can afford to do so now. However, this disturbs the long-term plans, especially financial plans. I have been hearing a debate for quite a while now where millennials are considering whether to live in a rental house all their lives and use the money on travel, adventure, etc. or to pay loan instalments for 20-30 years to get your own house. I personally think this is a choice of lifestyle people must make. If you are happy with moving around house to house in your post 60s age then sure do that, but will you really be able to do that?

We are a generation that was either studying or entered the workforce during the financial crisis which triggered a shift towards prioritising quality of life, experiences and adventure over money. I can’t count the number of times I have been tempted to try out a new restaurant with a fancy ambience or taking a short trip over the weekend just because I can afford to do so now. However, this disturbs the long-term plans, especially financial plans. I have been hearing a debate for quite a while now where millennials are considering whether to live in a rental house all their lives and use the money on travel, adventure, etc. or to pay loan instalments for 20-30 years to get your own house. I personally think this is a choice of lifestyle people must make. If you are happy with moving around house to house in your post 60s age then sure do that, but will you really be able to do that? I think a balanced lifestyle can be achieved because the good news is that we are a smart generation that has access to information instantly and have parents or elders that have done a commendable job on savings and efficient future planning. Take 1 to 2 days to figure out your current income and expenses and your future financial goals (doesn’t have to be very detailed as I am sure at this age it’s not easy to figure what you want to do 30-40 years down the line), 1 day to discuss with your parents to give you tips based on their experiences, 1 day to research on different financial tools to help you record your incomes & expenses and if required 1 to 2 days to find and meet with a good financial planner that will understand your goals and help you stay on path. These 6-7 days out of your whole “live in the moment” life – which most of us anyways spend on Facebook, Instagram, YouTube and Snapchat – will help you to keep living in the present and have a set strategy in place for your future as well.

I think a balanced lifestyle can be achieved because the good news is that we are a smart generation that has access to information instantly and have parents or elders that have done a commendable job on savings and efficient future planning. Take 1 to 2 days to figure out your current income and expenses and your future financial goals (doesn’t have to be very detailed as I am sure at this age it’s not easy to figure what you want to do 30-40 years down the line), 1 day to discuss with your parents to give you tips based on their experiences, 1 day to research on different financial tools to help you record your incomes & expenses and if required 1 to 2 days to find and meet with a good financial planner that will understand your goals and help you stay on path. These 6-7 days out of your whole “live in the moment” life – which most of us anyways spend on Facebook, Instagram, YouTube and Snapchat – will help you to keep living in the present and have a set strategy in place for your future as well.

Before we bought our home we decided that it was important to set out the financial ground work regarding what we needed to do in order to fund our loans, living expenses and at the same time able to save each week. So we sat down to determine what our repayments and bills would be once we moved into our home. From there we were able to work out the exact amount we were realistically able to save each week and made a commitment to put those funds aside without fail. Furthermore we made a commitment to put aside funds each week into our son’s bank account. Again this was a realistic figure and we stuck to it each week.

Before we bought our home we decided that it was important to set out the financial ground work regarding what we needed to do in order to fund our loans, living expenses and at the same time able to save each week. So we sat down to determine what our repayments and bills would be once we moved into our home. From there we were able to work out the exact amount we were realistically able to save each week and made a commitment to put those funds aside without fail. Furthermore we made a commitment to put aside funds each week into our son’s bank account. Again this was a realistic figure and we stuck to it each week.

Since July 1 2017, the ten percent employment rule regarding tax-deductible super contributions has been replaced. The rule meant that a person could not claim a tax deduction on personal Super Contributions if more than ten percent of their assessable income was obtained as an employee. The new rule is now any person under age 65 now may be able to claim a tax deduction on their contributions regardless of their employment arrangement, whilst those aged between 65 and 74 need to satisfy the Work Test in order to be eligible to make a contribution, and subsequently claim a tax deduction.

Since July 1 2017, the ten percent employment rule regarding tax-deductible super contributions has been replaced. The rule meant that a person could not claim a tax deduction on personal Super Contributions if more than ten percent of their assessable income was obtained as an employee. The new rule is now any person under age 65 now may be able to claim a tax deduction on their contributions regardless of their employment arrangement, whilst those aged between 65 and 74 need to satisfy the Work Test in order to be eligible to make a contribution, and subsequently claim a tax deduction.

With strawberries you need to have well drained soil, ideally planted in late winter/early spring, and when they start to fruit, you can’t have the strawberries touching the wet soil. Well I managed to have the correct set up and the strawberries began to grow. The kids ate the strawberries and we all lived happily ever after.

With strawberries you need to have well drained soil, ideally planted in late winter/early spring, and when they start to fruit, you can’t have the strawberries touching the wet soil. Well I managed to have the correct set up and the strawberries began to grow. The kids ate the strawberries and we all lived happily ever after.

One of the more prominent changes to Super that came into effect was the removal of the concessional tax treatment of Transition to Retirement Pensions (TTR Pension). Pre 1 July 2017 any money held within a TTR pension received a 0% tax rate on any income or realised capital gains, however post 1 July 2017 money held within the TTR pension is taxed at 15% (same as accumulation).

One of the more prominent changes to Super that came into effect was the removal of the concessional tax treatment of Transition to Retirement Pensions (TTR Pension). Pre 1 July 2017 any money held within a TTR pension received a 0% tax rate on any income or realised capital gains, however post 1 July 2017 money held within the TTR pension is taxed at 15% (same as accumulation).

With all the festivities and celebrations over and done with, for most of us it’s now time to pick up the pieces and start the New Year a fresh, which is a perfect time to review your personal insurance needs. Research from one of Australia’s largest personal insurance companies have found that only 37% of Aussies aged between 18-69 actually have life insurance and even more disturbingly only 18% have disability cover and income protection insurance. Further findings include how Australians are grossly underinsured. It’s estimated that the underinsurance gap in Australia is approximately $1.8 Billion, meaning there are a lot of Aussies out there who believe they have sufficient insurance cover, but in fact don’t. For most of us, we don’t like to think about insurance and when asked about how much we have, the first response is usually “I don’t know”.

With all the festivities and celebrations over and done with, for most of us it’s now time to pick up the pieces and start the New Year a fresh, which is a perfect time to review your personal insurance needs. Research from one of Australia’s largest personal insurance companies have found that only 37% of Aussies aged between 18-69 actually have life insurance and even more disturbingly only 18% have disability cover and income protection insurance. Further findings include how Australians are grossly underinsured. It’s estimated that the underinsurance gap in Australia is approximately $1.8 Billion, meaning there are a lot of Aussies out there who believe they have sufficient insurance cover, but in fact don’t. For most of us, we don’t like to think about insurance and when asked about how much we have, the first response is usually “I don’t know”.