Planning for Retirement – Is More than Just Having Enough Money

When we see a Retire Right client for the first time, often the most important question on their mind is “Have I got enough money to Retire?” Clearly becoming “Financially Free” is a critical component to a successful retirement but in our view it is only half the challenge.

Although the amount of money you have in retirement can determine the lifestyle you enjoy, an equally as important question is “What are you retiring to?”

We all understand what we’re retiring from, the 5 day 9 – 5 working work week (or maybe more), the early wake-ups and binge coffee drinking to get us through the day, the stress of work deadlines and the continual pile of work that magically appears on our desk day to day. When thinking of that, retirement seems like a dream come true, who wouldn’t want to retire?

But often a common occurrence is for people to struggle after the initial elation associated with having what seems to be a long holiday subsides. After longing for retirement for potentially up to 40 years there’s suddenly no routine, you’re now free 7 days a weeks, and there’s only so much Golf you can play, Netflix you can watch and you can’t mow the lawns or trims the hedges every day.

To quote a client, “my family knew I was battling when I stained the deck for a second time in 12 months”.

For many there is not only the battle of filling in your time, there is also the challenges associated with a sense of purpose and value. Once again for over 30 years peoples work has given them a sense of purpose in life and they have been valued, but in an instance this stop. The challenge is to replace work with activities that you enjoy and give you the same purpose.

Another often overlooked component of Retirement which we wrote about in our CPE article was the “Retired Husband Syndrome” and this is another challenge for many couples, particularly when one partner has developed their own social network and weekly routine while the other has been at work for the past 30 odd years.

Jenny is often heard telling clients that her mother told her father early on in his retirement “that she married him for better or for worse, but not for lunch”. Being around your partner 24/7 can often be a challenge for a couple until they form their own individual routine and activities.

These “non-financial” challenges often rear their heads 3, 6, 12 or 24 months down the track so in our view it is as critical to put strategies in place to overcome these challenges early to ensure that you are prepared, just like the strategies you put in place to overcome the financial challenges of Retirement.

Retirement can be the most exciting period of your life, for some they take it as an opportunity to take-up hobbies that they’ve put aside during their working life, learn something new like a second language, or even take a chance to try something they thought they never would or didn’t think they’d have the time too. You now have 7 days a week to do with what you will, and from our experiences, we find clients transition the best into retirement when they have a pre-determined view of what their retirement will look like. Clients who decide to “wing it” once work stops, generally find the transition much harder. In many instances those who have successfully transitioned into retirement are busier in retirement than they have ever been.

Thinking about retirement can be very daunting, and for most it all revolves around that question “Have I go enough money to Retire?” Our experience as a Retirement Coach for our clients highlights that this question isn’t what is most important, but instead mapping out your ideal retirement looks like, is the most critical, the rest just tends to follow.

So the challenge we throw out is to ask if you were to look back at yourself 20 years after retiring, what would have had to have happened for you to sit back and say that the last 20 years of my retirement has been fantastic!

– Warren Hanna –

One of the first things retirees quickly discover is that they have too much time on their hands with nothing to do. Playing a round of golf with mates or enjoying a drink at the bar will only fill up a certain amount of time in the day and you can’t go doing the same thing every day. Retired couples and singles alike will quickly become very unhappy once they run out of things to do.

One of the first things retirees quickly discover is that they have too much time on their hands with nothing to do. Playing a round of golf with mates or enjoying a drink at the bar will only fill up a certain amount of time in the day and you can’t go doing the same thing every day. Retired couples and singles alike will quickly become very unhappy once they run out of things to do.

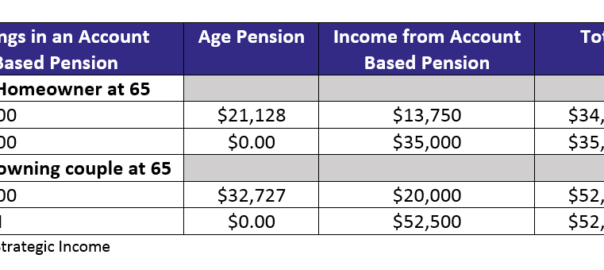

Unfortunately for some, the Age Pension will be critical to fund their retirement, but the Age Pension age doesn’t need to be your Retirement Age. There’s a few things you can do to help reduce your reliance on the Age Pension and retire when you want to retire, our motto is that we’d rather you be working because you want to, not because you have to.

Unfortunately for some, the Age Pension will be critical to fund their retirement, but the Age Pension age doesn’t need to be your Retirement Age. There’s a few things you can do to help reduce your reliance on the Age Pension and retire when you want to retire, our motto is that we’d rather you be working because you want to, not because you have to.

with an aggregate annual turnover of less than $10 million, you may be able to immediately deduct the cost of a depreciating asset that you purchase for less than $20,000. In order to access the deduction, the asset must be income producing for your business, purchased between 7:30PM on 12 May 2015 and 30 June 2018, and installed and ready for use before the end of the financial year. There is no limit to the number of eligible purchases that can be claimed.

with an aggregate annual turnover of less than $10 million, you may be able to immediately deduct the cost of a depreciating asset that you purchase for less than $20,000. In order to access the deduction, the asset must be income producing for your business, purchased between 7:30PM on 12 May 2015 and 30 June 2018, and installed and ready for use before the end of the financial year. There is no limit to the number of eligible purchases that can be claimed.